Producer Marketing Materials

Producer Video

Develop Your Retirement Planning Sales

Looking for a great way to help you increase sales? Consider the retirement planning strategy. The retirement planning strategy uses permanent life insurance to provide clients with death benefit protection while offering the potential to supplement their income during retirement.

Client Profile:

- Ages 30-60

- Need for life insurance protection

- Middle to high income earner

- Concerned about family’s financial needs if death occurs during work years

- Looking to supplement financial security in retirement years

- Self-employed, member of a partnership, or corporate-employed

Helpful Tips:

- Death benefit protection during both working years and retirement years. Cash values inside of a life insurance policy grow tax-deferred.1

- No income contribution limits and generally tax-free withdrawals and loans to the cost basis (assumes non-modified endowment contract status, or MEC).2,3,4,5

Sample Cases:

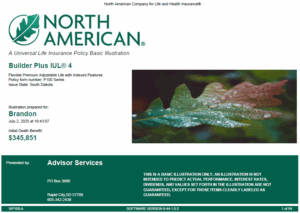

- Sample Case: Builder IUL

Brandon, age 38, had been maxing out his 401k and Roth IRA contributions and was looking for other ways to save for retirement. His advisor showed him the power of a non-qualified defined contribution life insurance supplemental retirement plan design, using the Builder Plus IUL from North American. Brandon will place $20,000 after-tax money towards the plan, to age 65. Then at age 66 he will begin tax-free distributions from the plan, which are estimated to be over $140,000 annually. Review this sample illustration to see this plan in action.

View illustration

1. The tax-deferred feature of universal life or indexed universal life insurance is not necessary for a tax-qualified plan. In such instances, your client should consider whether other features, such as the death benefit and optional riders make the policy appropriate for the client’s needs. Before purchasing a policy, your client should obtain competent tax advice both as to the tax treatment of the policy and the suitability of the product.

2. Financial Markets, Inc. does not give tax advice. Please advise your customers to consult with and rely on a qualified legal or tax advisor before entering into or paying additional premiums with respect to such arrangements.

IRS CIRCULAR 230 NOTICE

Any tax advice included in this written or electronic communication, including any attachments, was not intended or written to be used, and it cannot be used by you or any taxpayer for the purpose of avoiding any penalties that may be imposed on you or any other person under the Internal Revenue Code or applicable state or local tax law provisions. Although any tax advice contained herein was written to support the promotion or marketing of the transaction(s) matter(s) addressed by the advice, it cannot be used by you or any taxpayer to, promote, market or recommend to another party any transaction or matter addressed herein. Taxpayers should seek advice based on their particular circumstances from an independent tax advisor.

3. In some situations, loans and withdrawals may be subject to federal taxes. North American Company does not give legal or tax advice. Clients should be instructed to consult with and rely on their own tax advisor or attorney for advice on their specific situation.

4. Income and growth on accumulated cash values is generally taxable only upon withdrawal. Adverse tax consequences may result if withdrawals exceed premiums paid into the policy. Withdrawals or surrenders made during a Surrender Charge period will be subject to surrender charges and may reduce the ultimate death benefit and cash value. Surrender charges vary by product, issue age, sex, underwriting class, and policy year.

5. For most policies, withdrawals are free from federal income tax to the extent of the investment in the contract, and policy loans are also tax-free so long as the policy does not terminate before the death of the insured. However, if the policy is a Modified Endowment Contract (MEC), a withdrawal or policy loan may be taxable upon receipt. Further, unpaid loan interest on a MEC may be taxable. A MEC is a contract received in exchange for a MEC or for which premiums paid during a seven-year testing period exceed prescribed premium limits (7-pay premiums).

Consumer Marketing Materials

Statistics

• 61% of Baby Boomers are more scared of outliving their retirement assets than death.

• 93% of customers would leave an advisor if they don’t receive Social Security advice.

• A formal retirement plan is the biggest factor for how confident you clients feel about their retirement security, yet only 3 of 10 have one in place.

• 4 of 10 Americans believe no matter how much they save and how they invest they will not have enough money in retirement.

• Concerns about longevity are well founded: one of every four 65 year olds will live to age 90, and one out of ten will live to age 95.

• 50% of households are at risk of having their standard of living decline in retirement.

Dedicated Team

2026 fmiAgent Point Awards

You must be logged in to use this feature.